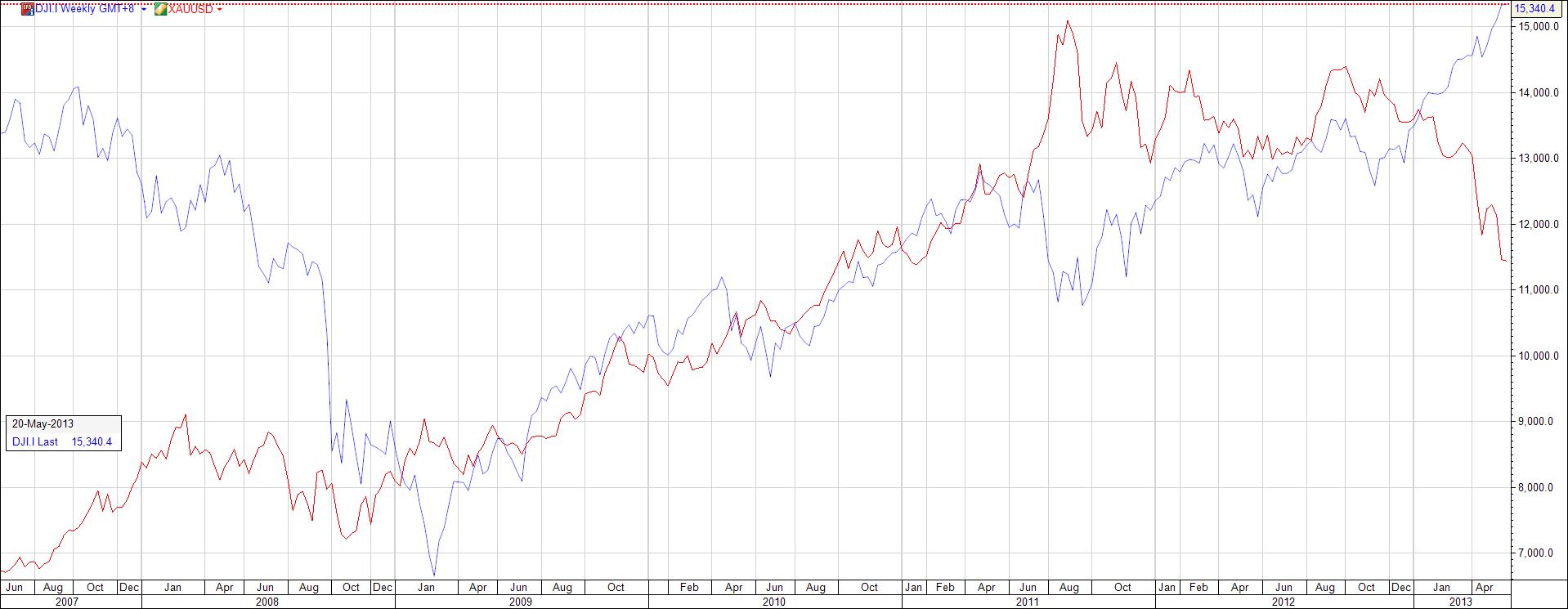

The above is a chart that superimposes both the gold price graph and the Dow Jones Index.

Generally, there is a negative correlation between gold and the equity markets.

During the boom years of 2006 and 2007, look at how poorly performing gold was, and we see it again during the latter part of 2011 and this year. Every time there is good economic data on the recovery of the economies and growth story, the price of gold will drop.

However, it is a reality today that gold is an asset class that is part of the asset allocation in an investor’s wealth portfolio. It is no longer looked upon as a traditional hedging instrument. It has come of his own in the past 12 years. Today, there is a deep enough and broad enough market, that is, sufficient retail, corporate, institutional and government are and have invested in gold.

Today, it could be argued that gold is a pseudo currency, it has liquidity, it has an underlying value and it can be used in trade. When the world is flush with liquidity and interest rates are low, confidence wanes in currencies as investors feel that the underlying value of the currency is weak, given that the global economies are weak, except for the emerging markets and Asia.

I believe the worse is over the the United States and for Euroland, there are still some bumps ahead, however, both economies have exhibited resilience and tenacity, they have turned the corner. Now, just because they have turned the corner does not mean that the road to economic growth will not have hiccups, it will and we should expect it.

We believe the medium term 3 year outlook for gold would be that it will find a base at about $1,000/-.

Right now, institutional investors, that is, the fund managers are all selling gold or calling for a sell in gold. The gold market is extremely bias short futures which will continue to add downward pressure to the price of gold.

What is the recommendation?

If you have gold holdings or gold ETFs, do consider rebalancing your asset allocation back to more equities. The outlook for equities is positive and yet dangerous.

Right now, equity markets are driven and supported by liquidity and not by fundamental growth in the economy nor healthy earnings from corporates.

If the transition to a healthier economy and strong corporate earnings happen when QE is pulled back and interest rates rises, than equity markets will continue to rise. If this transition is not handled properly, then, we may see some significant correction in the equity markets.